Hiring an insurance agent involves more than verifying a license. Employers need a screening program that covers criminal history, professional credentials, financial responsibility, and ongoing monitoring, built around the access risks of the role and the FCRA compliance requirements that apply when a consumer reporting agency is used.

Key Takeaways

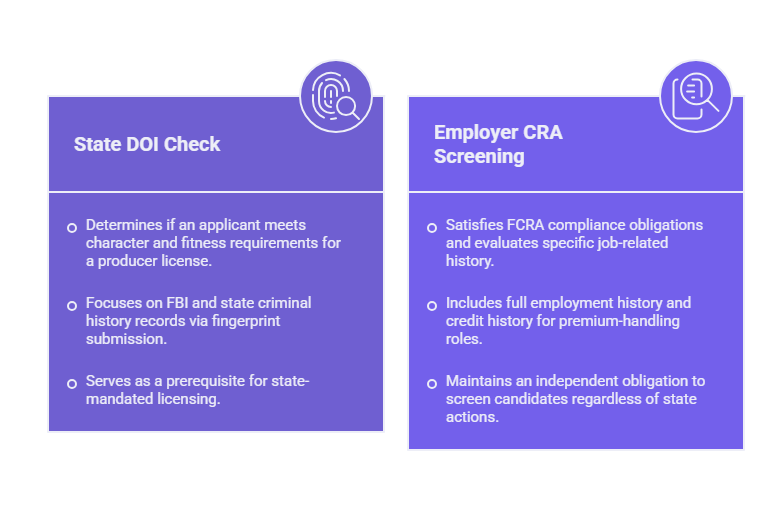

- A state DOI licensing background check and an employer background check serve different purposes. Passing a DOI licensing check does not satisfy the employer’s independent screening obligation.

- The screening stack for insurance agents scales with the access risk of the role. A licensed producer handling client premiums warrants a different depth of check than an administrative coordinator with no client contact.

- Professional license verification is a distinct check from the DOI licensing background check. It confirms current standing, active appointments, and any disciplinary history, and it should be run at hire and monitored on an ongoing basis.

- Credit history checks are appropriate for producers in roles involving premium handling, trust accounts, or fiduciary responsibility. Several states restrict employment credit checks, and the applicable restrictions must be confirmed before ordering.

- FCRA applies in full to every background check ordered through a consumer reporting agency on an insurance agent or producer, whether they are a direct employee or an independent contractor.

- Independent producers are not exempt from the employer’s screening obligations. Agencies and carriers that treat independent producer onboarding as a licensing transaction rather than an employment screening process create FCRA compliance gaps.

- Ongoing monitoring matters in insurance. A producer who acquires a disqualifying event after hire, whether a new criminal conviction, a license suspension, or a disciplinary action, may remain in the field undetected without a monitoring program in place.

- The adverse action process applies to producers as it does to any other workforce. A disqualifying background check result requires a FCRA-compliant pre-adverse and adverse action workflow before the decision is communicated.

Insurance employers often assume that the state DOI licensing process handles their screening obligations. It does not. The state licensing check is the regulator’s tool, designed to protect consumers by ensuring that producers meet the state’s character and fitness requirements to hold a license. It is not designed to satisfy the employer’s independent need to know who they are appointing to represent their business, handle client funds, and act under their authority.

A well-built insurance agent background check program addresses both: what the regulator requires and what the employer needs to make a defensible hiring decision. This guide covers the full screening stack, the access tiers that determine how deep each check should go, and the FCRA compliance requirements that apply regardless of how the screening obligation originates.

Who These Requirements Apply To

Background check requirements for insurance agents apply more broadly than most employers initially assume. The obligation is not limited to direct employees of a single carrier. It extends to captive agents, independent producers, brokers, managing general agents, adjusters, and subcontractors who represent an agency or carrier in the field.

The captive versus independent distinction matters less for screening purposes than it does for compensation and contract structure. Captive agents, as direct employees, typically move through a standard HR onboarding workflow that includes a background check as a routine step. Independent producers, by contrast, are often onboarded through a licensing or appointments team rather than HR. Their background check is frequently treated as a formality alongside license appointment, with the result that the FCRA compliance workflow, including standalone disclosure, written authorization, and the adverse action process, is either abbreviated or skipped entirely.

That treatment does not satisfy FCRA. When a consumer reporting agency is used to screen an independent producer, the same compliance requirements apply as for any direct employee. The employment classification of the individual does not create an exemption.

The Screening Stack: What a Complete Insurance Agent Background Check Includes

The right screening stack depends on the role. A producer with no client-facing responsibilities and no access to premium accounts warrants a different depth of check than a licensed producer managing client funds and transacting across multiple lines. Access risk, not job title, determines the appropriate scope.

| Check Type | Applies To | Notes |

| Criminal history search | All roles | National database plus county-level verification at current and prior addresses |

| Identity verification / SSN trace | All roles | Foundation for all other checks |

| Professional license verification | All licensed producers | Active status, appointments, disciplinary history |

| Sex offender registry search | All roles | All states, territories, and D.C. |

| Employment verification | All roles | Confirms prior positions and tenure |

| Education verification | Roles where credentials are a condition | Where a degree or certification is required |

| Employment credit report | Premium-handling and trust account roles | Separate FCRA disclosure required; state restrictions apply |

| FINRA BrokerCheck cross-reference | Dual-licensed producers | Required for securities-licensed individuals under FINRA Rule 3110 |

| Federal criminal search | All roles, recommended | Supplements state and county searches |

| MVR check | Roles involving client travel or transportation | Active license, violations, DUI history |

Each component addresses a distinct screening purpose and cannot be substituted by another check in the stack.

Criminal History

The criminal history search is the foundation of the insurance agent screening stack. A national database search alone is not sufficient. The national database aggregates records from multiple sources but functions as a pointer to jurisdictions, not a comprehensive record. County-level verification at current and prior addresses for the past seven years is the standard for surfacing records the national database would miss. For insurance roles involving access to client funds or sensitive personal information, a federal criminal search is also appropriate as a supplement.

Professional License Verification

License verification confirms that the producer’s license is active, in good standing, and not subject to any restriction affecting their ability to transact in the appointed lines. It also surfaces any disciplinary history, administrative orders, or suspensions on record with the state DOI. This is a different check from the DOI licensing background check run at initial licensure. License verification is an employer-side check of current status, and it should be run at hire and monitored on an ongoing basis for any change in standing.

Employment Credit Report

Credit checks are appropriate for producers in roles where financial responsibility is directly relevant: handling client premiums, managing trust accounts, or serving in roles with fiduciary exposure. FCRA requires a separate standalone written disclosure specifically for any credit check. That disclosure must be a document consisting solely of the disclosure and cannot be combined with any other document, including the general background check disclosure or the employment application. Several states restrict or prohibit employment credit checks for certain roles. Confirm which restrictions apply in each state where the producer will be employed or appointed before ordering, as this list has continued to expand in recent legislative cycles.

FINRA BrokerCheck

For producers who hold both an insurance license and a securities license, a BrokerCheck cross-reference is required under FINRA Rule 3110. BrokerCheck records disciplinary actions, regulatory proceedings, and employment history for registered representatives and investment advisers. It is a public database and should be part of any screening workflow for dual-licensed individuals.

State DOI Requirements and How They Interact With the Employer’s Screening Program

State DOI licensing background checks and employer background checks operate on parallel tracks. Understanding the interaction prevents two common compliance errors: assuming the DOI check covers the employer’s screening obligation, and assuming that licensing approval means the employer’s due diligence is complete.

What State DOI Background Checks Cover

Many states require resident producer applicants to submit fingerprints for FBI and state criminal history checks, either through NIPR or direct state DOI submission. Requirements vary by state, and the applicable process should be confirmed with the relevant state DOI. The DOI uses those results to determine whether the applicant meets the state’s character and fitness requirements to hold a producer license, checking on behalf of the regulator to protect consumers.

What State DOI Background Checks Do Not Cover

A DOI background check tells the regulator whether to grant a license. It does not satisfy the employer’s FCRA compliance obligations when a CRA is used, confirm the individual’s full employment history, or evaluate credit history for premium-handling roles. The employer’s independent screening obligation does not diminish because the state conducted its own check.

Nonresident Producer Considerations

Many states waive additional fingerprinting for nonresident producers who have already been fingerprinted in their home state. The nonresident appointment process through NIPR is typically faster and may involve less DOI-level screening than the resident process, depending on the state. An employer appointing a nonresident producer may therefore be relying on background check information that is older, from a different state’s standards, or conducted under different criteria than the employer’s own program would apply.

The Renewal Cycle Gap

State DOI licensing checks occur at initial application and at renewal cycles, typically every two years. A producer who acquires a disqualifying event between renewal cycles, whether a criminal conviction, a license action in another state, or a disciplinary finding, remains licensed until the next renewal. Only the employer’s independent monitoring program will surface this between cycles.

FCRA Compliance in Insurance Agent Screening

FCRA applies to every background check ordered through a consumer reporting agency on an insurance agent or producer, whether they are a direct employee or an independent contractor. The insurance regulatory framework does not modify or replace FCRA obligations. Both apply simultaneously, and three areas in particular create compliance gaps for insurance employers.

Disclosure and Authorization

Before ordering any CRA-based background check, the employer must provide a standalone written disclosure, separate from the employment application, the producer appointment agreement, and any other document, stating that a consumer report will be obtained for employment purposes. Written authorization must be obtained before the check is ordered. Many agencies skip this step for contractor producers, treating the onboarding as a licensing transaction rather than an employment screening process. That approach does not satisfy FCRA.

Adverse Action

When a background check result influences a decision not to hire, appoint, or continue working with a producer, FCRA’s two-step adverse action process applies. The process requires:

- A pre-adverse action notice with a copy of the consumer report and the CFPB Summary of Rights

- A reasonable opportunity for the individual to respond or dispute, typically interpreted as at least five business days, before the final decision is made

- A final adverse action notice if the organization proceeds, including the CRA’s name, address, and phone number, a statement that the CRA did not make the adverse decision, and notice of the producer’s right to obtain a free copy of the report within 60 days

Even when a result may be disqualifying under applicable licensing law, FCRA notice requirements are not eliminated. The adverse action workflow applies regardless of how the underlying disqualification is characterized.

Independent Contractors

The employment classification of the individual does not change FCRA applicability. An independent producer whose consumer report is used in a decision about their appointment is entitled to the same FCRA protections as a direct employee. Agencies that maintain separate onboarding workflows for contractors and employees should confirm that FCRA compliance steps are applied consistently across both populations.

FCRA compliance requirements vary by state and circumstance. This section is informational only and does not constitute legal advice. Consult qualified legal counsel before implementing or modifying your background check program.

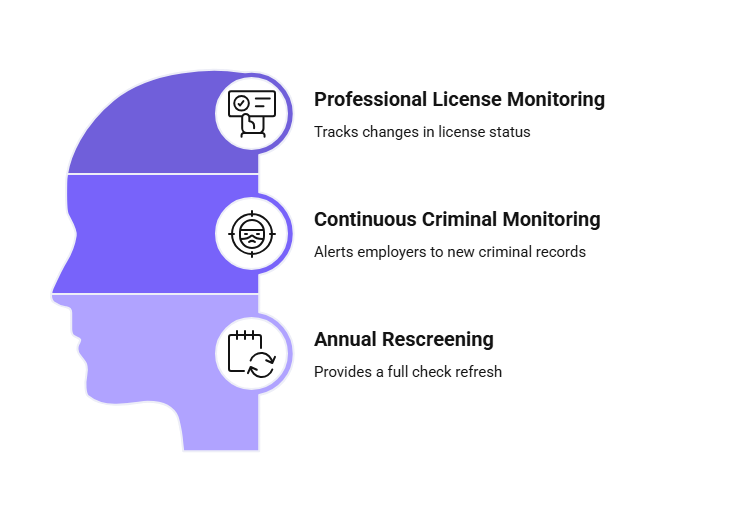

Ongoing Monitoring: Why the Screening Program Does Not End at Appointment

A background check completed at hire or appointment reflects the producer’s record on that date only. It provides no coverage for criminal convictions, license actions, or disciplinary findings that occur afterward. In insurance, where producers operate with ongoing client access and often handle sensitive financial transactions, the post-hire gap carries real exposure. Three mechanisms address it.

Professional License Monitoring

License status can change between credentialing cycles. A producer whose license is suspended in a secondary state, who receives a disciplinary action from a licensing board, or whose appointment is restricted may remain in the field without detection unless the employer has a monitoring program in place. Professional license monitoring watches licensing board systems for status changes including suspensions, revocations, probationary conditions, and disciplinary actions, and generates alerts when a change is detected.

Continuous Criminal Monitoring

Continuous criminal monitoring enrolls cleared producers in ongoing record surveillance and generates alerts when new criminal records appear in monitored databases, typically within days of a new filing. For insurance employers, this is the mechanism that surfaces a new disqualifying conviction between scheduled rescreening cycles. Without it, the employer has no way to learn of a post-hire conviction until the next annual check, a license renewal, or a self-disclosure.

Annual Rescreening

Annual rescreening provides a comprehensive scope refresh, re-running the full check stack on a defined cycle. For producers, aligning annual rescreening with license renewal cycles is a practical operational anchor that keeps the compliance record current and creates a natural documentation checkpoint.

Conclusion

A complete insurance agent background check program is not a single check run at appointment. It is a layered stack that matches check depth to access risk, applies FCRA compliance requirements consistently across direct employees and independent producers, and maintains ongoing monitoring to surface disqualifying events that occur after hire. The state DOI licensing process handles the regulator’s obligation. The employer’s screening program handles everything else.

Frequently Asked Questions

What background checks are required for insurance agents?

A complete stack includes criminal history with county-level verification, professional license verification, identity verification, and a sex offender registry search for all roles. Employment credit reports are appropriate for producers handling premiums or trust accounts. A FINRA BrokerCheck cross-reference is required for dual-licensed producers. All checks ordered through a CRA must follow FCRA disclosure, authorization, and adverse action requirements.

Does a felony prevent someone from selling insurance?

It depends on the nature of the conviction and applicable state licensing requirements. State DOIs evaluate felony convictions as part of the character and fitness review for licensing eligibility. The specific offenses that trigger a licensing bar vary by state. Consult applicable state DOI guidance and qualified legal counsel.

Do independent insurance agents need a background check?

Yes. FCRA requirements apply to independent contractors when a CRA is used, not just direct employees. Agencies and carriers that appoint independent producers without running a FCRA-compliant background check, including required disclosure, authorization, and adverse action procedures, are exposed under FCRA regardless of the producer’s classification.

What crimes disqualify someone from working in insurance?

Disqualifying offenses vary by state. Most state DOIs apply a character and fitness standard that considers the nature of the offense, the time elapsed, and evidence of rehabilitation. Crimes involving fraud, dishonesty, breach of fiduciary duty, and financial crimes are commonly evaluated more strictly for insurance roles. State DOI licensing guidance for each applicable jurisdiction should be reviewed.

Does FCRA apply to insurance producer background checks?

Yes. When a consumer reporting agency is used, FCRA requires a standalone written disclosure and written authorization before the check is ordered. The full two-step adverse action process applies if the result influences a negative employment or appointment decision. This requirement applies to independent contractors as well as direct employees.

How often should insurance agents be rescreened?

Annual rescreening aligned with license renewal cycles is the recognized operational standard. Continuous criminal monitoring and professional license monitoring between scheduled rescreening cycles are the mechanisms that surface new disqualifying events before the next annual check.

What is professional license verification and why does it matter for insurance hiring?

Professional license verification confirms that a producer’s license is currently active, in good standing, and free of restrictions or disciplinary actions. It is distinct from the DOI licensing background check run at initial licensure. License status can change between renewal cycles, and monitoring for changes is a standard component of an ongoing insurance agent screening program.

Additional Resources

- NAIC Producer Licensing Background Checks Resource

https://content.naic.org/cipr-topics/producer-licensing - Background Checks: What Employers Need to Know (FTC / EEOC Joint Guidance)

https://www.ftc.gov/tips-advice/business-center/guidance/background-checks-what-employers-need-know - EEOC Enforcement Guidance: Consideration of Arrest and Conviction Records in Employment Decisions

https://www.eeoc.gov/laws/guidance/enforcement-guidance-consideration-arrest-and-conviction-records-employment-decisions - FINRA BrokerCheck

https://brokercheck.finra.org - NIPR Producer Licensing Information

https://nipr.com

ABOUT THE CREATOR

Charm Paz, CHRP

Recruiter & Editor

Charm Paz is an HR professional at GCheck, specializing in background screening, fair hiring, and regulatory compliance. She holds from the Professional Background Screening Association (PBSA) and helps organizations navigate employment regulations with clarity and confidence.

With a background in Industrial and Organizational Psychology, she translates policy into practice to build ethical, compliant, human-centered hiring systems that strengthen decision-making over time.