Employment verification for freelancers requires adapting traditional background check methods to accommodate decentralized work arrangements where standard employer confirmation is unavailable. Organizations must evaluate alternative documentation such as 1099 forms, contracts, invoices, and platform records to construct verifiable work histories while understanding that freelance verification centers on engagement proof rather than hierarchical tenure.

Key Takeaways

- Freelancers, independent contractors, and self-employed individuals operate outside traditional employment structures, requiring modified verification approaches that account for client-based rather than employer-based work relationships.

- Documentable work history for contingent workers prioritizes evidence of completed engagements and income receipt over supervisor references or organizational tenure.

- A documentation hierarchy ranging from IRS 1099-NEC forms to client letters and payment records helps organizations assess verification confidence levels based on available proof.

- Client references differ fundamentally from employment verification, as references evaluate work quality while verification confirms engagement existence and duration.

- Tax documentation serves as the closest analog to W-2 employment records but presents timing limitations and privacy considerations that affect verification workflows.

- Platform-based freelance work through digital marketplaces creates third-party verification opportunities with inherent access restrictions and data completeness gaps.

- Verification rigor should align with role sensitivity and specific risk factors rather than applying uniform standards across all contractor engagements.

- Internal policies that define acceptable documentation types, escalation procedures for verification gaps, and compliance recordkeeping requirements enable consistent contractor screening.

Understanding Classification Differences: Contractor, Employee, and Self-Employed Status

The foundation of effective employment verification for freelancers begins with understanding how independent contractors differ from traditional employees in work structure and legal classification. These distinctions directly affect what documentation exists and which verification methods apply.

Legal Classification Framework

Independent contractors maintain control over how they complete work, provide their own tools and resources, and typically serve multiple clients simultaneously. The IRS applies common-law rules examining behavioral control, financial control, and relationship type to determine worker classification.

Key classification distinctions include:

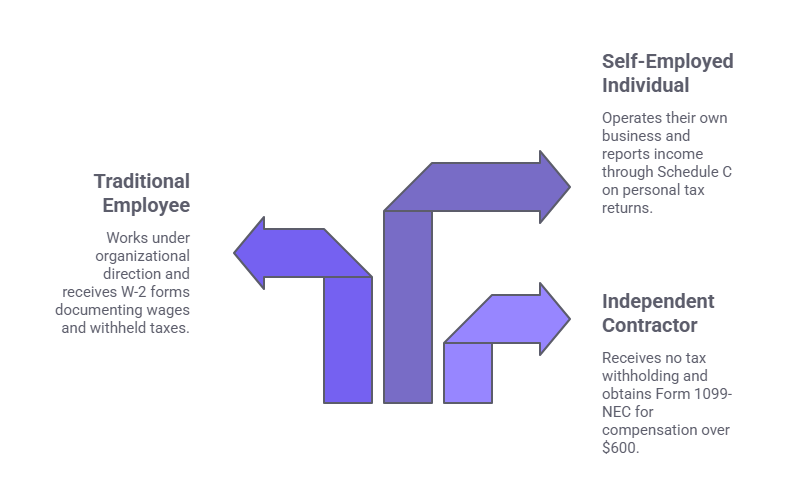

- Independent contractors receive no tax withholding and obtain Form 1099-NEC when annual compensation exceeds $600

- Traditional employees work under organizational direction and receive W-2 forms documenting wages and withheld taxes

- Self-employed individuals operate their own businesses and report income through Schedule C on personal tax returns

Organizations exercise greater control over when, where, and how employees perform their duties compared to contractor relationships.

As a recruiter, I have worked with many freelancers who have made a name for themselves through freelance work, and one of the first things that becomes apparent is that traditional verification methods don’t give us a full picture of the candidate. After all, where are they supposed to get verified from? It’s a critical point to make because, as a recruiter, the way we verify a candidate directly impacts the way we hire them and the fairness of the process. However, if we move away from intangible concepts of work and focus on actual deliverables, we get a much clearer picture of a candidate’s capabilities. The way we change verification methods in today’s hiring environment isn’t just a process change; it’s a way to stay relevant.

Implications for Work History Documentation

These classification differences determine what records exist for verification purposes. Employees generate personnel files, performance reviews, and payroll records maintained by HR departments. Contractors generate invoices, service agreements, and project deliverables but lack centralized employment records. Self-employed individuals may have business registration documents, professional licenses, and client contracts but no single authoritative employment record.

Understanding classification helps verification teams set appropriate expectations about documentation availability and identify which alternative verification methods suit specific work arrangements.

Classification Verification as Preliminary Step

Organizations should be aware that worker misclassification creates legal compliance risks separate from verification accuracy. When converting contractors to employees or when classification questions arise, organizations should consult legal counsel to evaluate whether working relationships were properly classified, as classification determinations involve complex legal analysis of multiple factors.

Redefining Work History in Freelance Contexts

Traditional employment verification confirms job titles, dates of employment, and sometimes compensation through employer HR departments. Verifying independent contractor work history requires reframing what constitutes meaningful work history when centralized employers do not exist.

Engagement-Based Rather Than Tenure-Based History

Freelancer work history verification focuses on confirming that specific client engagements occurred, deliverables were completed, and compensation was received. Unlike employee tenure representing continuous organizational affiliation, contractor work history consists of discrete projects or ongoing service arrangements with defined scopes. A freelancer's five-year work history might encompass thirty separate client relationships rather than one or two employer affiliations.

Deliverable Completion as History Marker

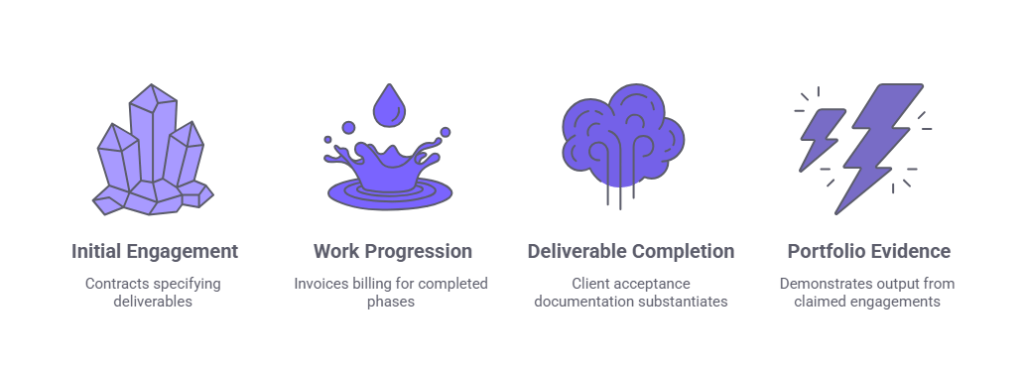

For project-based freelance work, deliverable completion serves as a meaningful history marker:

- Contracts specifying deliverables provide initial engagement documentation

- Invoices billing for completed work phases mark project progression

- Client acceptance documentation substantiates deliverable completion

- Portfolio evidence demonstrates output from claimed engagements

Organizations verifying freelancer work history should evaluate whether claimed engagements produced documentable deliverables and whether available records substantiate completion.

Income Patterns as Continuity Evidence

Unlike salaried employment with predictable pay periods, freelance income varies based on project timing, client payment terms, and work volume fluctuations. Sequential tax documents spanning multiple years demonstrate work continuity even when individual client engagements change frequently. Verification processes should account for income variability that reflects legitimate freelance work patterns rather than interpreting gaps as employment discontinuity.

Documentation Hierarchy: Evaluating Proof Quality

Organizations need frameworks for assessing freelance work documentation quality, recognizing that some evidence types provide stronger verification confidence than others.

Tier One: Tax Documents and Official Forms

IRS Form 1099-NEC is generally issued when a payer organization remits $600 or more in non-employee compensation to a recipient during a calendar year, subject to IRS reporting requirements and exceptions. This form confirms payer identity, recipient taxpayer identification, annual compensation amount, and tax year.

Additional tax documentation includes:

- Form 1099-K issued by payment settlement entities for transactions exceeding reporting thresholds

- Schedule C from personal tax returns detailing self-employment business income and expenses

- IRS wage and income transcripts providing authoritative verification of reported income

Organizations have no legal right to access personal tax returns and may only review Schedule C when candidates voluntarily choose to provide this documentation. Organizations can verify 1099-NEC authenticity through IRS wage and income transcripts when candidates authorize and provide these documents, or when candidates grant permission through IRS Form 4506-T allowing transcript release to third parties.

Tier Two: Contracts and Service Agreements

Written contracts between freelancers and clients document engagement terms including scope, deliverables, compensation, and duration. Signed agreements provide strong verification evidence, particularly when contracts include specific start dates, project milestones, and payment schedules.

Master service agreements establishing ongoing contractor relationships may span multiple years with individual project work orders defining specific engagements. Both framework agreements and detailed project contracts serve verification purposes, though specific project documentation offers more granular engagement confirmation.

Tier Three: Invoices and Payment Records

Invoices issued by freelancers to clients document services provided, dates of service, amounts billed, and payment terms. Sequential invoices covering extended periods demonstrate ongoing client relationships and provide detailed engagement timelines. Payment records including bank statements showing client deposits, payment platform transaction histories, or cancelled checks corroborate invoice documentation.

Organizations should note that invoice and payment documentation requires voluntary disclosure by freelancers, as third parties cannot access banking records without authorization.

Tier Four: Client Letters and References

Letters from clients confirming engagement details offer qualitative verification evidence. Unlike reference letters evaluating work quality, verification letters should specifically confirm engagement existence, duration, and nature of services. Organizations requesting client verification letters should provide templates specifying required information elements to ensure letters address verification needs.

Some clients cannot or will not provide written confirmation due to confidentiality policies, legal considerations, or administrative constraints.

Tier Five: Portfolio Work and Public Evidence

For creative, technical, or professional service freelancers, completed work portfolios demonstrate capabilities and substantiate claimed project experience. While portfolios confirm work was produced, they provide limited verification of client relationships, compensation, or engagement timing without corroborating documentation.

Client References Versus Employment Verification

Organizations frequently conflate reference checks with employment verification when evaluating freelance work history. Understanding the distinction helps verification teams gather appropriate information and avoid relying on references to fulfill verification functions.

Functional Differences Between References and Verification

Reference checks assess work quality, professional capabilities, interpersonal skills, and performance outcomes through subjective evaluations from previous clients or colleagues. Employment verification confirms objective facts about work relationships including engagement dates, services contracted, project completion, and sometimes compensation.

For freelancers, client references serve traditional reference check functions but cannot substitute for verification documentation. A glowing reference confirms a client was satisfied with work quality but does not necessarily provide the engagement date specificity, compensation confirmation, or documentation formality that verification processes require.

When Client Contact Serves Verification Purposes

Direct client contact can fulfill verification needs when clients confirm specific factual information about engagement timing, scope, and completion. Verification-focused client contact should request confirmation of contractor name, approximate engagement start and end dates, general services provided, and whether the freelancer completed contracted work.

Platform and Agency Intermediaries

Freelancers working through staffing agencies, creative agencies, or project placement firms may have limited direct client contact, as agencies serve as intermediaries contracting with end clients. In these arrangements, agencies may provide verification while end clients remain unknown to freelancers. Platform-based freelance work creates similar intermediary situations where platforms mediate client relationships.

Documentation When References Are Unavailable

Client unavailability for verification purposes occurs frequently in freelance contexts due to business closures, contact information changes, client relocations, confidentiality restrictions, or clients who were individuals rather than organizations with ongoing operations. Freelancers unable to provide client references should present alternative documentation from higher tiers in the verification hierarchy, such as contracts, invoices with corresponding payment records, or tax documentation covering engagement periods in question.

Tax Documents as Employment Verification Proxies

IRS Form 1099-NEC and related tax documents serve as the closest freelance equivalent to W-2 employment verification, though important limitations affect their utility in verification processes.

What 1099-NEC Forms Confirm

Form 1099-NEC documentation includes the following verification elements:

- Payer organization name, address, and taxpayer identification number

- Recipient contractor information and tax identification

- Non-employee compensation amount of $600 or more

- Calendar year for which compensation was paid

This documentation verifies that a financial relationship existed between payer and recipient during the specified tax year and that compensation reached reporting thresholds. Organizations can verify 1099-NEC authenticity through IRS wage and income transcripts when candidates authorize and provide these documents, or when candidates grant permission through IRS Form 4506-T allowing transcript release to third parties.

Limitations of Tax Document Verification

Tax forms operate on calendar year cycles with filing deadlines extending months after year-end. For recent freelance work, 1099-NEC forms may not yet exist even for legitimate completed engagements.

Key limitations include:

| Limitation | Impact on Verification | Mitigation Strategy |

| $600 reporting threshold | Small engagements generate no 1099-NEC | Request contracts and payment records |

| Annual reporting cycle | Current-year work lacks documentation | Accept invoices and interim records |

| Limited granularity | No project details within tax year | Supplement with engagement-specific documentation |

Form 1099-K and Payment Platform Documentation

Payment processors and third-party settlement organizations issue Form 1099-K when payment volume exceeds reporting thresholds. For freelancers receiving most compensation through platforms like PayPal or payment processors, 1099-K forms substantiate business income existence during specific periods. When combined with platform transaction details, this documentation can verify payment timing and amounts for specific clients.

Organizations should recognize that 1099-K reporting thresholds have been subject to regulatory changes. The IRS has announced plans to lower reporting thresholds, though implementation timelines have been adjusted. Organizations should verify current 1099-K reporting requirements as thresholds may affect which freelance income generates documentation.

Privacy Considerations with Tax Documentation

Tax returns and related documents contain sensitive financial information beyond specific employment verification needs. Organizations requesting tax documentation must limit requests to specific forms needed for verification purposes and implement secure handling, storage, and disposal procedures that comply with federal and state requirements for protecting sensitive tax information. Unauthorized disclosure or inadequate safeguarding of tax records may result in legal liability.

Platform-Based Work and Digital Marketplace Verification

The growth of freelance platforms including Upwork, Fiverr, Toptal, and specialized industry marketplaces creates new verification opportunities and challenges as digital intermediaries maintain engagement records traditionally held by employers or clients.

What Platform Records Document

Freelance platforms document user profiles, project histories, client reviews, earnings summaries, and engagement timelines for work conducted through platform systems. Platform work histories typically include project titles, client feedback, completion dates, and sometimes earnings amounts depending on privacy settings and platform policies.

Many platforms provide exportable work history reports, earnings summaries, or verification letters confirming user account standing and general engagement information.

Access Limitations and Privacy Controls

Platform work records belong to individual freelancers subject to platform privacy policies and terms of service. Organizations cannot directly access freelancer platform profiles or detailed work histories without explicit consent and cooperation from the freelancer. Some platforms offer third-party verification services allowing authorized background check providers to access work history data. These services require explicit user consent and authorization through platform-specific processes. Organizations must ensure candidate authorization complies with FCRA requirements when platform data will be used for employment decisions.

Platform Verification Reliability

Established freelance platforms implement identity verification, payment processing, and user accountability measures that enhance work history reliability compared to unverified self-reported information. However, platform accounts may be subject to manipulation through prohibited practices including review fraud, account sharing, or misrepresenting engagement details. Organizations should understand each platform's identity verification and authentication processes before determining appropriate reliance levels for verification purposes.

Platform marketplace work represents legitimate employment history even though it occurs outside traditional employer relationships.

Limitations of Platform Work History

Freelancers typically maintain work relationships both through platforms and through direct client arrangements. Platform records document only platform-mediated work, potentially representing a fraction of total freelance activity. Comprehensive verification requires evaluating both platform and off-platform engagement documentation. Some platforms focus on specific project types, skills, or industry sectors, meaning freelancers may maintain profiles across multiple platforms for different work types.

Risk Considerations Specific to Contractor Work History

Organizations verify employment history to assess various risks including candidate misrepresentation, employment gap explanations, credential validation, and role-specific security or compliance requirements.

Misrepresentation and Fabrication Risks

Decentralized freelance work with limited third-party verification creates opportunities for work history fabrication or embellishment. Candidates might inflate engagement duration, invent client relationships, exaggerate compensation, or misrepresent project scope and responsibilities.

The absence of centralized HR departments maintaining authoritative records means verification relies more heavily on candidate-provided documentation subject to potential manipulation. Organizations should assess documentation authenticity through multiple corroborating sources rather than accepting single evidence types. Tax documentation provides stronger fraud resistance than invoices or contracts that candidates could potentially create.

Skills Validation Versus Engagement Confirmation

Employment verification confirms that work relationships existed but does not validate skills or capabilities. For freelancers claiming specialized expertise, organizations may need separate skills assessment processes beyond work history verification. Portfolio reviews, skills testing, technical interviews, or trial projects serve skills validation functions distinct from confirming that freelancers previously worked with specific clients.

Employment Gap Analysis

Traditional employment verification identifies gaps between jobs that might raise questions about candidate activities during unemployment periods. Freelance work often involves intentional flexibility with variable project timing, creating natural gaps that differ from involuntary unemployment. Organizations should recognize that intermittent project work represents normal freelance patterns rather than concerning employment gaps.

Role Sensitivity and Verification Rigor Matching

Organizations should calibrate freelance work history verification rigor based on role sensitivity, access levels, and specific risk factors. Positions involving financial authority, data access, vulnerable populations, or security clearances warrant more thorough verification than roles with limited risk exposure.

For sensitive positions, organizations might require multiple documentation types for each claimed engagement, conduct direct client verification when possible, and verify tax documentation through IRS transcripts. Establishing tiered verification approaches allows organizations to manage verification costs and administrative burden while maintaining appropriate diligence for risk levels.

Compliance and Regulatory Requirements

Some industries impose regulatory requirements for workforce screening including contractors and temporary workers. Financial services, healthcare, transportation, and other regulated sectors may mandate specific verification elements regardless of worker classification. Organizations in regulated industries should verify specific requirements applicable to their sector and jurisdiction, as requirements vary by regulatory framework and may extend to all workforce members including contractors.

Building Internal Policies for Contractor Verification

Systematic approaches to employment verification for freelancers require documented policies that establish verification requirements, acceptable documentation types, escalation procedures for verification gaps, and recordkeeping protocols.

Defining Verification Triggers and Scope

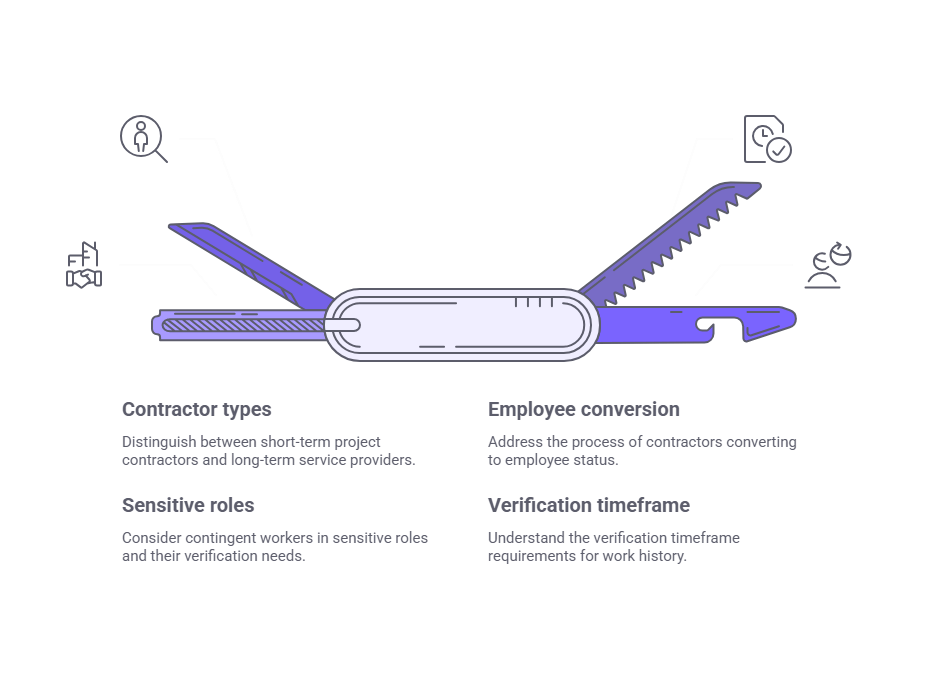

Organizations should specify which contractor arrangements trigger work history verification requirements. Policy considerations include:

- Short-term project contractors versus long-term service providers

- Contractors converting to employee status

- Contingent workers in sensitive roles

- Verification timeframe requirements for work history

Clear scope parameters help verification teams apply consistent standards. Some organizations verify only the most recent or longest contractor engagements while others require comprehensive work history documentation.

Acceptable Documentation Matrix

Policies should enumerate acceptable documentation types for contractor verification organized by evidence strength. A comprehensive matrix addresses:

| Verification Scenario | Preferred Documentation | Alternative Documentation |

| Domestic contractor with major clients | 1099-NEC forms plus payment records | Contracts plus client verification letters |

| Platform-based freelancer | Platform work history reports | Platform earnings summaries plus tax forms |

| International contractor | Contracts plus payment records | Foreign tax documents plus client letters |

| Long-term self-employment | Multi-year Schedule C documentation | Business registration plus client contracts |

Comprehensive documentation policies reduce case-by-case decision-making and promote verification consistency. Organizations might establish documentation alternatives allowing candidates to satisfy verification requirements through multiple pathways.

Verification Gap Escalation Procedures

Documentation gaps occur frequently in freelance verification due to client unavailability, missing records, confidentiality restrictions, or informal work arrangements. Policies should establish escalation procedures defining how verification teams handle incomplete documentation. Some organizations implement risk-based gap tolerance, accepting documentation limitations for lower-risk roles while requiring complete verification for sensitive positions.

When verification concerns contribute to hiring decisions that negatively affect candidates, organizations using consumer reporting agencies must follow FCRA adverse action procedures, including pre-adverse action notices providing candidates opportunity to dispute information, and final adverse action notices if decisions proceed.

Candidate Communication and Transparency

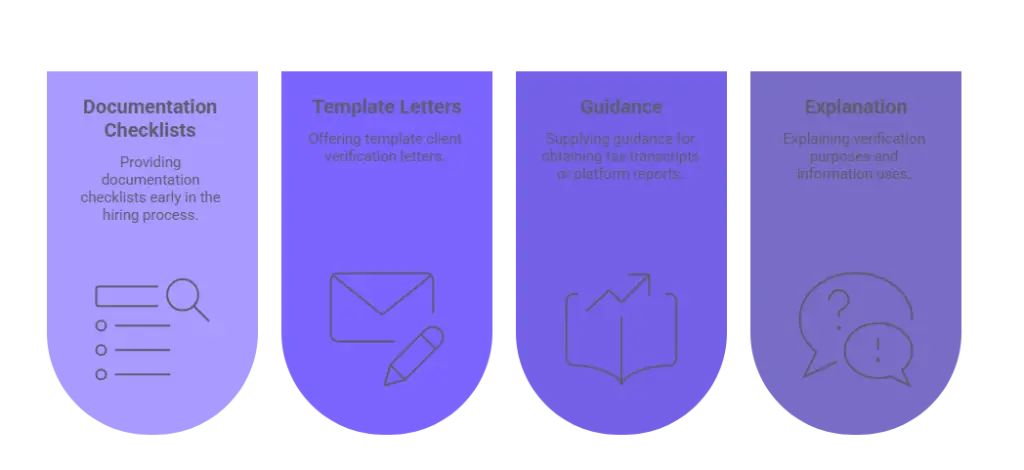

Verification policies should address how organizations communicate contractor verification requirements to candidates. Effective communication practices include:

- Providing documentation checklists early in the hiring process

- Offering template client verification letters

- Supplying guidance for obtaining tax transcripts or platform reports

- Explaining verification purposes and information uses

Proactive candidate support accelerates verification completion and reduces back-and-forth requests. Transparency about verification purposes builds candidate trust and cooperation.

Compliance Recordkeeping Requirements

Organizations must maintain verification documentation to demonstrate compliance with background check requirements, support adverse action procedures when applicable, and provide audit trails for regulatory reviews. Federal and state laws may impose specific retention requirements for background check documentation. Verification records containing tax information, financial details, or other sensitive data require enhanced security measures and limited access.

Conclusion

Employment verification for freelancers requires adapting traditional confirmation processes to accommodate decentralized work arrangements, alternative documentation types, and engagement-based rather than tenure-based work histories. Organizations that develop systematic verification approaches utilizing tax documentation, contracts, payment records, and platform work histories while calibrating verification rigor to role-specific risks can effectively validate contractor work backgrounds. Clear policies defining acceptable documentation, escalation procedures for verification gaps, and compliance recordkeeping enable consistent contractor screening that balances thoroughness with practical constraints.

Frequently Asked Questions

Do I need to verify every freelance project a candidate lists on their resume?

Organizations should establish policies specifying verification scope based on role requirements and risk factors. Most verification approaches focus on primary or recent engagements representing substantial portions of work history rather than attempting to confirm every project.

Can I require candidates to provide complete tax returns to verify freelance work?

Organizations may request specific tax forms like 1099-NEC documents relevant to employment verification, but requiring complete personal tax returns raises privacy concerns and may exceed legitimate verification needs. Some jurisdictions restrict employer access to tax returns or limit permissible uses.

Is LinkedIn profile history sufficient verification for freelance work?

Professional networking profiles constitute candidate self-reported information without independent verification. While profiles may corroborate claimed work history, they do not provide the documentation rigor that contracts, tax forms, payment records, or client verification letters offer.

What should I do when a candidate's freelance clients are out of business or unreachable?

Client unavailability occurs frequently in contractor verification and should not automatically disqualify candidates. Organizations should request alternative documentation such as contracts from the original engagement, invoices with corresponding payment records, or tax forms showing the client as payer.

How do I verify international freelance work for candidates who worked with foreign clients?

International contractor arrangements may not generate U.S. tax documentation, requiring alternative verification approaches. Organizations should request contracts or service agreements, payment records showing international transfers, foreign tax documents when applicable, or platform records for international marketplace work.

Can I skip work history verification if a contractor is converting to employee status after working with my organization?

Internal knowledge of contractor work quality during previous engagements does not substitute for verifying work history claims about engagements with other organizations. However, organizations may reasonably limit verification scope to work history outside the current organization since internal records already document the known contractor relationship.

What verification approach works for freelancers who work primarily through multiple gig platforms?

Platform-based freelancers should provide work history reports, earnings summaries, or verification documentation from each major platform where they maintain active work histories. Organizations should request platform documentation covering verification time periods and may need to aggregate information across multiple platforms.

Are there legal limits on what I can ask freelance candidates to document about past work?

Organizations must comply with Fair Credit Reporting Act requirements when using consumer reporting agencies or third-party background check providers to obtain employment verification information. Additionally, multiple states and localities prohibit employers from requesting salary or compensation history information during hiring processes, with restrictions that may apply to contractor compensation inquiries.

Additional Resources

- Independent Contractor (Self-Employed) or Employee?

https://www.irs.gov/businesses/small-businesses-self-employed/independent-contractor-self-employed-or-employee - Instructions for Forms 1099-MISC and 1099-NEC

https://www.irs.gov/instructions/i1099mec - Employment Eligibility Verification (I-9 and E-Verify)

https://www.uscis.gov/i-9-central - A Summary of Your Rights Under the Fair Credit Reporting Act

https://www.consumer.ftc.gov/articles/pdf-0096-fair-credit-reporting-act.pdf - Using Consumer Reports: What Employers Need to Know

https://www.ftc.gov/business-guidance/resources/using-consumer-reports-what-employers-need-know

ABOUT THE CREATOR

Charm Paz, CHRP

Recruiter & Editor

Charm Paz is an HR and compliance professional at GCheck, working at the intersection of background screening, fair hiring, and regulatory compliance. She holds both FCRA Core and FCRA Advanced certifications through the Professional Background Screening Association (PBSA) and supports organizations in navigating complex employment regulations with clarity and confidence.

With a background in Industrial and Organizational Psychology and hands-on experience translating policy into practice, Charm focuses on building ethical, compliant, and human-centered hiring systems that strengthen decision-making and support long-term organizational health.