INDUSTRY GUIDES

Discover the unique challenges of Colorado fintech background checks, balancing state privacy laws and federal regulations effectively.

Created by

Reviewed by

Colorado's fintech sector requires sophisticated background screening that balances traditional financial regulations with evolving state privacy laws and cannabis-related compliance complexities. This comprehensive guide addresses the unique challenges HR leaders face when conducting compliant background checks in Colorado's financial technology landscape, where federal FCRA requirements intersect with state-specific regulations and the SAFE Act mandates for money services businesses.

Colorado has emerged as a significant fintech hub. Denver ranks among the top ten cities for financial technology innovation. The state's regulatory environment creates a complex backdrop for employment screening, where traditional banking oversight converges with progressive technology policies and unique state-level consumer protections.

Colorado fintech companies operate under dual regulatory frameworks. Traditional financial institutions face established background check requirements from federal agencies like the FDIC, OCC, and Federal Reserve. Meanwhile, innovative fintech startups—particularly those offering payment processing, digital lending, or cryptocurrency services—navigate evolving guidance from state regulators and the Colorado Division of Banking.

This regulatory intersection demands sophisticated screening approaches. A payment processing startup may need SAFE Act compliance for certain roles, while simultaneously adhering to Colorado's consumer data privacy expectations that exceed federal minimums. Companies offering banking-as-a-service must implement screening protocols that satisfy partner bank requirements while maintaining compliance with employment law.

The Colorado Consumer Credit Reporting Act establishes state-level protections that complement federal FCRA requirements. Key differences include stricter adverse action notice timelines and enhanced consumer dispute rights. Colorado also restricts salary history inquiries under the Equal Pay for Equal Work Act, which intersects with background verification processes when confirming employment history.

Colorado's marijuana legalization since 2012 has created unique screening challenges. While cannabis remains federally illegal—a significant concern for fintech companies dealing with federal banking regulations—Colorado law prohibits employment discrimination based solely on lawful off-duty marijuana use. Financial services employers must carefully balance federal compliance obligations with state employment protections.

The Bank Secrecy Act and USA PATRIOT Act impose background screening obligations on financial institutions. These regulations require reasonable efforts to verify employee identity and assess potential risks related to money laundering or terrorist financing. For mortgage-related fintech, the SAFE Act mandates comprehensive background checks, including fingerprint-based FBI criminal history reports for mortgage loan originators. FINRA and SEC regulations affect fintech companies operating in investment or securities spaces, requiring Form U4 disclosures and ongoing monitoring.

Comprehensive background screening for Colorado financial services positions extends beyond basic criminal history checks. The multi-faceted approach addresses regulatory requirements, protects company reputation, and mitigates financial crime risks inherent to the industry. Each component serves specific compliance purposes while contributing to holistic risk assessment.

| Screening Component | Typical Timeline | Primary Purpose |

| County Criminal Search | 2-4 business days | Identify local convictions and pending charges |

| State Criminal Repository | 1-3 business days | Statewide conviction verification via CBI |

| Federal Criminal Search | 3-5 business days | Detect federal offenses including financial crimes |

| Employment Verification | 3-7 business days | Confirm work history and detect resume fraud |

| Education Verification | 2-5 business days | Validate degrees and professional certifications |

| Credit History Check | 1-3 business days | Assess financial responsibility for relevant roles |

| FBI Fingerprint Check | 2-4 weeks | Required for SAFE Act MLO compliance |

Different positions require varying screening depths based on risk profiles. Entry-level roles typically receive standard criminal and identity verification, while senior positions undergo comprehensive screening including credit checks and professional reference verification.

Criminal background checks form the foundation of fintech screening programs. For Colorado-based searches, employers typically conduct county-level criminal record searches supplemented by statewide repository checks through the Colorado Bureau of Investigation. Federal courthouse searches may be necessary for positions with significant fiduciary responsibility or regulatory requirements.

The seven-year reporting limitation under FCRA applies to most positions. However, financial institutions often qualify for FCRA exemptions when hiring for positions with salaries exceeding $75,000, allowing reporting of older records. Colorado's Fair Chance Act restricts when employers can inquire about criminal history, generally prohibiting questions until after initial application review.

In financial services, innovation may drive growth, but trust is what sustains it. In the context of increased speed of operations and developments in technology, the role of understanding who has access to critical information and financial processes only becomes more important. While background screening might be seen as part of the compliance process, the value behind it comes in terms of enabling the organization to make informed decisions ahead of time. Growth and governance don’t need to contradict one another, as the best organizations realize their reliance on one another.

Financial services regulations require robust identity verification, particularly for BSA compliance. Colorado fintech companies typically verify Social Security numbers and confirm identity documentation. Enhanced verification protocols apply to positions with access to customer financial data or transaction processing authority.

Credit history checks remain legally permissible in Colorado for financial industry positions. The state requires separate disclosure and authorization specifically for credit checks. Employers must demonstrate legitimate business needs, which courts generally recognize for roles involving financial responsibility or access to financial information.

Verification of stated qualifications protects against resume fraud, which studies suggest affects approximately 40% of applications. Colorado employers should verify degrees, professional licenses, and employment history—particularly for roles requiring specific financial certifications. The National Student Clearinghouse provides efficient degree verification for most U.S. institutions, while FINRA's BrokerCheck and NMLS Consumer Access databases offer public verification of financial professional credentials.

Mortgage-focused fintech companies face stringent requirements under the SAFE Act. This federal legislation established mandatory registration and state licensing for mortgage loan originators following the 2008 financial crisis. Colorado mortgage companies must facilitate comprehensive screening processes while ensuring individual MLOs meet all federal and state requirements.

All MLOs operating in Colorado must register through the Nationwide Multistate Licensing System and comply with Colorado Division of Real Estate requirements. The registration process includes comprehensive background screening that employers must facilitate, though individual applicants bear ultimate responsibility for submission. The SAFE Act background check includes fingerprint-based FBI criminal history reports, credit history review, and administrative sanctions screening.

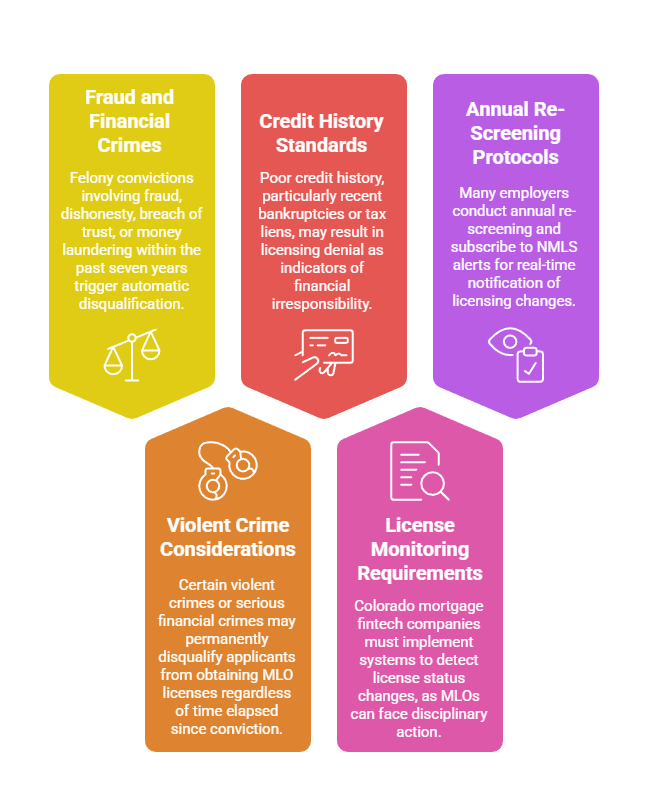

The SAFE Act establishes specific disqualifying criminal convictions that permanently or temporarily bar MLO licensing. Consider the following key disqualifiers and compliance obligations:

These requirements apply throughout the employment relationship. Companies hiring MLOs must verify current licensing status continuously and may not employ individuals whose licenses are suspended, revoked, or lapsed.

Colorado's legalized marijuana industry creates unique intersections with financial technology. Fintech companies serving cannabis businesses or considering Colorado-specific policies must navigate conflicting federal and state frameworks. The tension between state legalization and federal prohibition presents ongoing compliance challenges.

Colorado's Lawful Off-Duty Activities Statute prohibits employers from terminating or refusing to hire individuals based on lawful activities conducted off-premises during non-working hours. Court interpretations have extended these protections to marijuana use outside work, despite federal prohibition. For fintech companies, this creates tension with federal financial regulations and Drug-Free Workplace requirements for federal contractors.

Employers should clearly define safety-sensitive positions where impairment risks justify drug testing. Positions involving federal compliance oversight, BSA responsibilities, or partner bank relationships may justify stricter drug-free policies. However, Colorado counsel should review such determinations to ensure they meet legal standards.

Colorado has sealed hundreds of thousands of marijuana-related criminal convictions following legalization. These sealed records should not appear in properly conducted background checks. Individuals need not disclose sealed convictions during application processes.

Fintech employers may encounter pre-legalization marijuana convictions that haven't been sealed. The Colorado Chance to Compete Act suggests employers should carefully consider the relevance of older marijuana convictions to current financial services positions. This consideration applies particularly for offenses that would be legal under current state law.

Colorado's evolving data privacy framework adds compliance layers beyond traditional background screening regulations. The state implements comprehensive consumer privacy legislation that affects how employers collect, process, and retain background check information. Fintech companies must understand these intersections to maintain full compliance.

The Colorado Privacy Act, effective July 2023, establishes consumer rights regarding personal data collection and processing. While employment data receives partial exemptions, fintech companies must understand CPA intersections with background screening. This includes data retention, consumer access rights, and processing limitations.

Background check information collected during hiring creates ongoing data governance obligations. Companies should establish retention schedules that balance regulatory requirements with privacy principles favoring minimal data retention. Unsuccessful candidates may request access to collected personal data, requiring systems to retrieve and provide background screening information when requested.

The Fair Credit Reporting Act establishes federal standards for background screening. Colorado's Consumer Credit Reporting Act supplements FCRA with additional protections. Understanding both frameworks ensures complete compliance with disclosure, authorization, and adverse action requirements.

Colorado fintech employers must provide clear, standalone disclosure before conducting background checks. Separate written authorization is required, with specific additional disclosure for credit reports. When background information contributes to adverse employment decisions, employers must follow precise procedures including pre-adverse action notice, reasonable dispute time (typically five business days), and final adverse action notice if proceeding with the negative decision.

Most fintech companies partner with consumer reporting agencies for background screening. Colorado employers remain legally responsible for vendor compliance. Service agreements should specify compliance responsibilities, data security protocols, and accuracy guarantees. Regular vendor audits should assess ongoing compliance, particularly regarding permissible purposes and proper handling of consumer disputes.

As Colorado fintech companies grow from startups to mid-market enterprises, screening programs must scale appropriately. Strategic program design balances thoroughness with candidate experience and time-to-hire pressures. Effective programs adapt to company growth while maintaining consistent compliance standards across all hiring activities.

Not all positions require identical screening depth. Risk-based approaches categorize roles by regulatory requirements, financial access levels, and data sensitivity. Document the business justification for screening components applied to each role category to demonstrate compliance with fair hiring laws.

| Position Category | Screening Components | Rationale |

| Entry-Level Customer Service | Criminal history, identity verification, employment history | Limited financial access; focus on honesty and basic eligibility |

| Financial Analysts | Criminal history, credit check, education verification, professional references | Financial data access requires enhanced financial responsibility assessment |

| Compliance Officers | Comprehensive criminal history, credit check, sanctions screening, continuous monitoring | Regulatory oversight role demands highest scrutiny and ongoing verification |

| Senior Executives | Full comprehensive screening, board-level references, media searches | Fiduciary responsibility and reputational impact justify maximum due diligence |

| Mortgage Loan Originators | SAFE Act compliant screening with FBI fingerprints, credit, NMLS verification | Federal licensing requirements mandate specific comprehensive protocols |

Review categorizations periodically, particularly when launching new products or services. Position risk profiles may change as company offerings evolve.

Financial regulations increasingly expect ongoing monitoring beyond point-of-hire background checks. Many Colorado fintech companies implement continuous criminal monitoring that alerts employers to new criminal activity affecting current employees. Federal sanctions list monitoring should occur regularly for positions with BSA responsibilities.

Re-screening programs must comply with FCRA's requirement for new authorization before conducting subsequent background checks. Annual or biennial re-screening typically applies to positions with significant financial responsibility, compliance functions, or roles requiring maintained licensing. Clear policies should govern how new information discovered through monitoring will be evaluated and addressed.

Comprehensive documentation protects against compliance challenges and discrimination claims. Maintain detailed records throughout the screening process to demonstrate consistent policy application and regulatory compliance. Proper documentation serves as critical evidence in potential legal disputes or regulatory audits.

Key documentation requirements include:

The EEOC requires retaining hiring records for at least one year, with extended three-year retention for federal contractors. Other regulations may impose longer retention periods for specific industries or position types.

Background screening frequently reveals information requiring careful evaluation before making final hiring decisions. Colorado's fair chance hiring principles and FCRA requirements mandate individualized assessments. Employers must apply consistent evaluation frameworks while considering role-specific relevance of discovered information.

When background checks reveal potentially disqualifying information, employers must conduct individualized assessments. EEOC guidance emphasizes considering the nature and gravity of the offense, the time elapsed since the offense or completion of sentence, and the nature of the job sought. Colorado law reinforces these individualized assessment obligations through fair chance hiring legislation.

Document the assessment process thoroughly to demonstrate compliance and defend against potential discrimination claims. Consider whether the revealed information relates to specific job duties—for example, fraud convictions clearly relate to positions handling customer funds. Decade-old minor offenses may not impact current suitability for many fintech roles, particularly when balanced against rehabilitation evidence.

FCRA's adverse action process protects consumer rights while giving employers structure for defensible decisions. These procedures must be followed precisely to maintain compliance. The multi-step process ensures candidates have opportunities to identify and correct inaccurate information before final employment decisions.

First, provide pre-adverse action notice including a copy of the background report and the FTC's Summary of Consumer Rights. Wait a reasonable period—typically five business days—before issuing final adverse action to allow dispute processes. If proceeding with the decision after this period, provide final adverse action notice identifying the consumer reporting agency and confirming the candidate's right to dispute report accuracy. Colorado's shorter dispute resolution timeframes mean employers should allow adequate time before finalizing hiring decisions.

The background screening landscape continues evolving rapidly. Regulatory developments, technological advances, and changing social attitudes affect best practices for Colorado fintech employers. Forward-thinking companies monitor these trends to adapt screening programs proactively rather than reactively responding to compliance challenges.

AI-powered screening tools promise efficiency but raise accuracy and discrimination concerns. The EEOC has signaled increased scrutiny of algorithmic hiring tools that may produce disparate impact on protected classes. Colorado's tech-forward reputation may drive early adoption of AI governance standards affecting employment screening.

Fintech companies adopting AI screening tools should conduct disparate impact analyses and maintain human oversight of automated decisions. Vendors offering AI-enhanced screening should provide validation studies and adverse impact data demonstrating their tools don't create unlawful discrimination. Transparency about algorithmic factors builds candidate trust while supporting compliance with emerging AI regulations.

Colorado's Fair Chance Act restricts criminal history inquiries during initial application stages. Ongoing legislative trends suggest potential expansion of these restrictions or enhanced protections for individuals with criminal histories. Progressive screening policies can provide competitive advantages in Colorado's tight labor market by expanding talent pools.

Companies might delay criminal history checks until conditional offer stages. Eliminating automatic disqualifications for offenses unrelated to financial services duties demonstrates commitment to second-chance employment. These voluntary policies exceed current legal minimums while supporting inclusive hiring practices aligned with Colorado's progressive employment culture.

Fintech innovations are transforming identity verification methods. Open banking frameworks may enable employment verification through direct payroll system connections rather than traditional manual processes. Blockchain-based credential verification could streamline education and certification confirmation while reducing fraud risks through tamper-proof verification systems.

Colorado fintech companies at the forefront of these technologies should ensure new verification methods comply with FCRA requirements. Innovative verification approaches must provide transparency about information sources and allow consumers to dispute inaccurate data. Maintaining the consumer protections underlying traditional background screening regulations remains essential even as verification technologies advance.

Colorado fintech background checks require sophisticated approaches that balance multiple regulatory frameworks. HR leaders must design screening programs addressing industry-specific risks while complying with FCRA, CCCRA, and Colorado fair hiring principles. As fintech innovation continues and regulatory frameworks evolve, successful companies will build flexible screening protocols that protect compliance and company reputation. Partnering with qualified screening vendors and maintaining current knowledge of Colorado's unique regulatory landscape positions fintech employers for sustainable growth in one of America's most dynamic financial technology markets. With ever-growing regulatory requirements, screening can no longer be viewed merely as an independent HR task but as a key element within the framework of enterprise risk management. Companies that view their screening process in terms of trust and governance will find themselves better positioned to grow successfully.

Colorado fintech companies must conduct background checks based on role-specific regulatory requirements and company risk assessments. Most positions require criminal history screening at county and state levels, identity verification, and employment verification. Roles with financial responsibility often include credit checks with proper disclosure and authorization. Mortgage loan originators require SAFE Act compliant screening including fingerprint-based FBI checks, while positions with BSA compliance duties typically require enhanced due diligence including sanctions database screening and ongoing monitoring.

Colorado law prohibits employment discrimination based on lawful off-duty marijuana use, creating tension with federal financial regulations. Fintech employers should clearly identify safety-sensitive positions or roles with federal compliance responsibilities where drug-free requirements have documented business necessity. Pre-legalization marijuana convictions may be sealed in Colorado and shouldn't appear in proper background checks. Employers should consult legal counsel when developing drug testing and background screening policies to balance state employment protections with federal financial regulatory expectations.

The Fair Credit Reporting Act requires employers to provide clear, standalone written disclosure before conducting background checks and obtain separate written authorization from candidates. Before taking adverse action based on background information, employers must provide pre-adverse action notice including a report copy and summary of rights. Allow reasonable time for dispute (typically five business days), then provide final adverse action notice if proceeding with the negative decision. Colorado's Consumer Credit Reporting Act adds stricter dispute resolution timeframes that employers must follow.

Standard criminal and employment verification typically completes within 3-7 business days for Colorado searches. Fingerprint-based FBI checks required for SAFE Act compliance generally take 2-4 weeks. Timeline variations depend on county court processing speeds, previous residence locations requiring out-of-state searches, and education verification complexity. Fintech companies should build realistic timelines into hiring workflows, typically planning for 7-10 business days for standard screening and 3-4 weeks for comprehensive screening including federal database searches.

Yes, Colorado employers may implement continuous criminal monitoring programs that alert to new criminal activity affecting current employees. However, FCRA requires new authorization before conducting subsequent background checks, so companies should obtain appropriate ongoing monitoring consent during onboarding. Continuous monitoring is increasingly common for positions with financial responsibility, compliance functions, or regulatory licensing requirements. Programs should include clear policies about how new information will be evaluated and should apply individualized assessment principles before taking adverse employment action.

The Fair Credit Reporting Act establishes federal minimum standards for background screening, while Colorado's Consumer Credit Reporting Act adds state-level protections. Key Colorado differences include shorter timeframes for consumer reporting agencies to investigate disputes and additional consumer rights regarding information accuracy. Colorado fintech employers must comply with both federal FCRA and state CCCRA requirements, applying the stricter standard when laws differ. Both laws require separate disclosure and authorization before conducting background checks.

Legal requirements apply based on company activities and roles rather than company size or maturity. However, practical implementation often differs—early-stage startups may conduct basic screening while established companies implement sophisticated risk-based programs with continuous monitoring. Companies with bank charters, those offering money transmission services, or firms with federal regulatory oversight face stricter requirements regardless of size. As fintech startups scale and add regulated services, background screening programs should evolve to address growing regulatory obligations and risk profiles.

Remote employees working from Colorado require compliance with Colorado employment and background screening laws even if the employer is based elsewhere. For Colorado-based fintech companies hiring remote workers in other states, screening programs must comply with both Colorado and the employee's work location laws. This multi-state compliance often requires partnership with consumer reporting agencies experienced in nationwide screening and state-specific requirements. Remote hiring typically includes enhanced identity verification with particular attention to document authenticity.

Meet the GCheck Editorial Team, your trusted source for insightful and up-to-date information in the world of employment background checks. Committed to delivering the latest trends, best practices, and industry insights, our team is dedicated to keeping you informed.

With a passion for ensuring accuracy, compliance, and efficiency in background screening, we are your go-to experts in the field. Stay tuned for our comprehensive articles, guides, and analysis, designed to empower businesses and individuals with the knowledge they need to make informed decisions.

At GCheck, we're here to guide you through the complexities of background checks, every step of the way.

Contact us today for efficient, FCRA-compliant screening solutions

designed to keep your hiring process moving safely and smoothly.

LEGAL DISCLAIMER: The information provided in this article is for general informational and educational purposes only and should not be construed as legal advice or a substitute for consultation with qualified legal counsel. While we strive to ensure accuracy, employment screening laws and regulations—including but not limited to the Fair Credit Reporting Act (FCRA), Equal Employment Opportunity Commission (EEOC) guidelines, state and local ban-the-box laws, industry-specific requirements, and other applicable federal, state, and local statutes—are subject to frequent changes, varying interpretations, and jurisdiction-specific applications that may affect their implementation in your organization. Employers and screening decision-makers are solely responsible for ensuring their background check policies, procedures, and practices comply with all applicable laws and regulations relevant to their specific industry, location, and circumstances. We strongly recommend consulting with qualified employment law attorneys and compliance professionals before making hiring, tenant screening, or other decisions based on background check information.